Have you planned for an extended health care need?

You’ve spent time, effort and money devising a financial plan and retirement savings strategies to insure your nest egg and lifestyle security for the years ahead when career concerns no longer define, limit and govern your time.

You’ve spent time, effort and money devising a financial plan and retirement savings strategies to insure your nest egg and lifestyle security for the years ahead when career concerns no longer define, limit and govern your time.

The desire for choice, independence and self determination don’t retire when we do. We all want to be the boss of our new life’s adventure when the time comes, so there’s one more critical step to take to protect the fruits of all that planning…

. . . a plan for Long Term Health Care

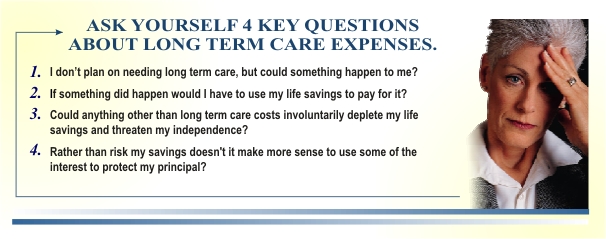

The Baby-Boomers have reshaped American economic life. Their impending retirements will bring profound economic opportunities. At Cornerstone Benefit & Retirement Group, Inc. we are committed to working with baby-boomers in preparation for active aging, long productive lives in retirement, and the need to plan for the possible illnesses and disabilities requiring extended health care.

Long Term Care Insurance is certainly an option for many, but it’s not the only option. There are other financial products which can protect your plans, and that’s what this is all about. Long Term Care Planning is planning that protects all the other planning you’ve done to insure your post-retirement lifestyle against the unexpected burden of financing an extended health care need.

Taxation & Long Term Care Insurance

| TABLE 1 | ||||

| Entity | Deductibility | Income Reporting | Discrimination Rules | Tax Treatment of Benefits |

| Individual | The lesser of the Premium or the Eligible Premium from Table 2. Medical Expenses are deductible to the extent they exceed 7.5% of Adjusted Gross Income. | N/A | N/A | Tax-Free |

| Self-Employed | Percentage from Table 2 of the lesser of Premium or Eligible Premium is deductible as a business expense. The remaining percentage is included as a Medical Expense under the 7.5% rule. | No | None | Tax-Free |

| S Corporations Partnerships LLC’s |

Same as self-employed | The portion of the Premium paid by the entity on behalf of a partner is included in the partner’s income. | None | Tax-Free |

| C Corporations | The entire Premium is fully deductible by the corporation. | No | None | Tax-Free |

Frequently Used Long Term Care Terms

To help in understanding long-term care and long-term care insurance, below are general explanations of some frequently used terms. The exact definitions of these terms can vary from company to company, from state to state, and from policy form to policy form, even between forms of the same company. Always consult the actual policy for the meaning of the terms applicable to your situation.

Activities of Daily Living (ADLs): Everyday functions and activities people usually are able to do without help. Includes bathing, continence, dressing, eating, toileting and transferring (moving in or out of a bed, chair or wheelchair).

Adult Day Care: Care provided during the day for adults, usually outside of the home in a group setting.

Assisted Living Facility: A residential living arrangement that can provide individualized care and health services for residents who need assistance with Activities of Daily Living. May also be called Custodial Care, Domiciliary Care, Intermediate Care, Personal Care, Residential Health Care, Sheltered Care or Supported Care Facilities.

At-Home Care: Services and supplies provided when living in one’s home, such as Home Health Care, Adult Day Care, Hospice Care and Respite Care.

Caregiver Training: An instructional program for the training of an informal caregiver (Husband, wife, adult child or other relative or friend) whose caregiving will allow a patient to remain at home instead of entering a long-term care facility. This type of training is typically provided by home health care agencies or other Qualified Home Health Care Providers, nursing homes, hospitals or other health care agencies or professionals.

Cognitive Impairment: A deficiency in a person’s memory; orientation as to person, place or time; deductive or abstract reasoning; or judgment as it relates to safety awareness.

Custodial Care (Also called Personal Care): Care to help people perform Activities of Daily Living that can be provided by someone without professional medical training.

Elimination Period: The length of time for which a long-term care insurance policy will not pay benefits for services covered by a policy. The longer the elimination period, the lower the premium.

Exclusions: The types of expenses that are not covered by a policy.

Functional Incapacity: A person’s inability to perform a number of those Activities of Daily Living specified in a Long-Term Care insurance policy.

Guaranteed Renewable: Means that an insurance policy cannot be cancelled, terminated, changed or reduced if all renewal premiums are paid on time, except rates may be revised by the carrier on a class basis.

Home Health Aide: A licensed or certified home care worker, other than a doctor, nurse or therapist, who assists patients in performing the Activities of Daily Living.

Home Health Care: A variety of services and supplies provided in the home, such as visits by nurses, Home Health Aides and physical, occupational, speech and inhalation therapists, Homemaker Services, drugs, medicines, medical supplies and lab services as well as durable portable therapeutic equipment.

Home Health Care Provider: A person or organization licensed or certified to provide Home Health Care services.

Homemaker Services: Includes domestic, laundry and cleaning services; food shopping and errands; meal preparation and cleanup and transportation assistance to and from medical appointments.

Hospice Care: Care provided for pain and symptom management associated with a terminal illness and any related conditions. Normally provided by an agency that specializes in providing pain relief, symptom management and support services to dying persons and their families.

Intermediate Care: Occasional nursing and rehabilitative care performed by, or under the supervision of, skilled medical personnel.

Inflation Protection: An insurance policy option that calls for regular increases in benefit limits to help offset the future increases in long-term care expenses.

Married Couple or Married Person Discount: A reduction in the insurance policy premium when both spouses have Long-Term Care coverage.

Medically Necessary Care: Services and supplies which are provided in accordance with accepted medical practice; and as are required by the patient’s condition. It doesn’t include care that exceeds the scope, duration or intensity needed to provide safe, adequate and appropriate care; nor does it include treatment provided solely for someone’s convenience.

Paid-up Survivorship: An insurance policy option that will waive the surviving spouse’s future premiums upon the death of the other spouse. A minimum duration of continuous coverage under the policy by both spouses may be required in order for the benefit to be applicable.

Respite Care: Professional care provided on a short-term basis for the purpose of temporarily relieving unpaid caregivers, such as family members or friends.

Restoration of Benefits: An insurance policy feature that will bring a policy’s maximum benefit amounts back to the level that would apply if policy benefits hadn’t been paid.

Skilled Nursing Care: Daily nursing and rehabilitative care that can be performed only by, or under the supervision of, skilled medical personnel.

Tax-Qualified Long-Term Care Insurance Policy: A policy that conforms to certain standards in federal law offering federal income tax advantages.

Third Party Notice (Authorized Designee): An insurance policy feature that lets the policyholder name someone who the insurance company would notify if the policy is about to lapse because the premium hasn’t been paid on time.

Waiver of Premium: An insurance policy feature that suspends the premium payment requirement while policy benefits are being paid.